What the Series Has Established

This is the sixth and final post in the Exit by Design series. Across the previous five, we established a set of ideas that build on one another. Every government contracting owner will eventually exit their business. The Five Ds represent the most common ways that exit happens before the owner is ready. There are six primary exit paths available, each with its own requirements and tradeoffs. The choice of path should be shaped by what the owner wants to preserve, and the financial outcome is only one dimension of that question.

This post brings those threads together. It examines the full arc of exit by design: what the timeline actually looks like, what the work involves at each stage, and where to begin if the conversation has not yet started.

The Timeline Is Longer Than Most Owners Expect

One of the most consistent miscalculations in exit planning is the assumption that the process begins when the owner decides to sell. By that point, many of the decisions that determine the quality of the outcome have already been made — or foreclosed.

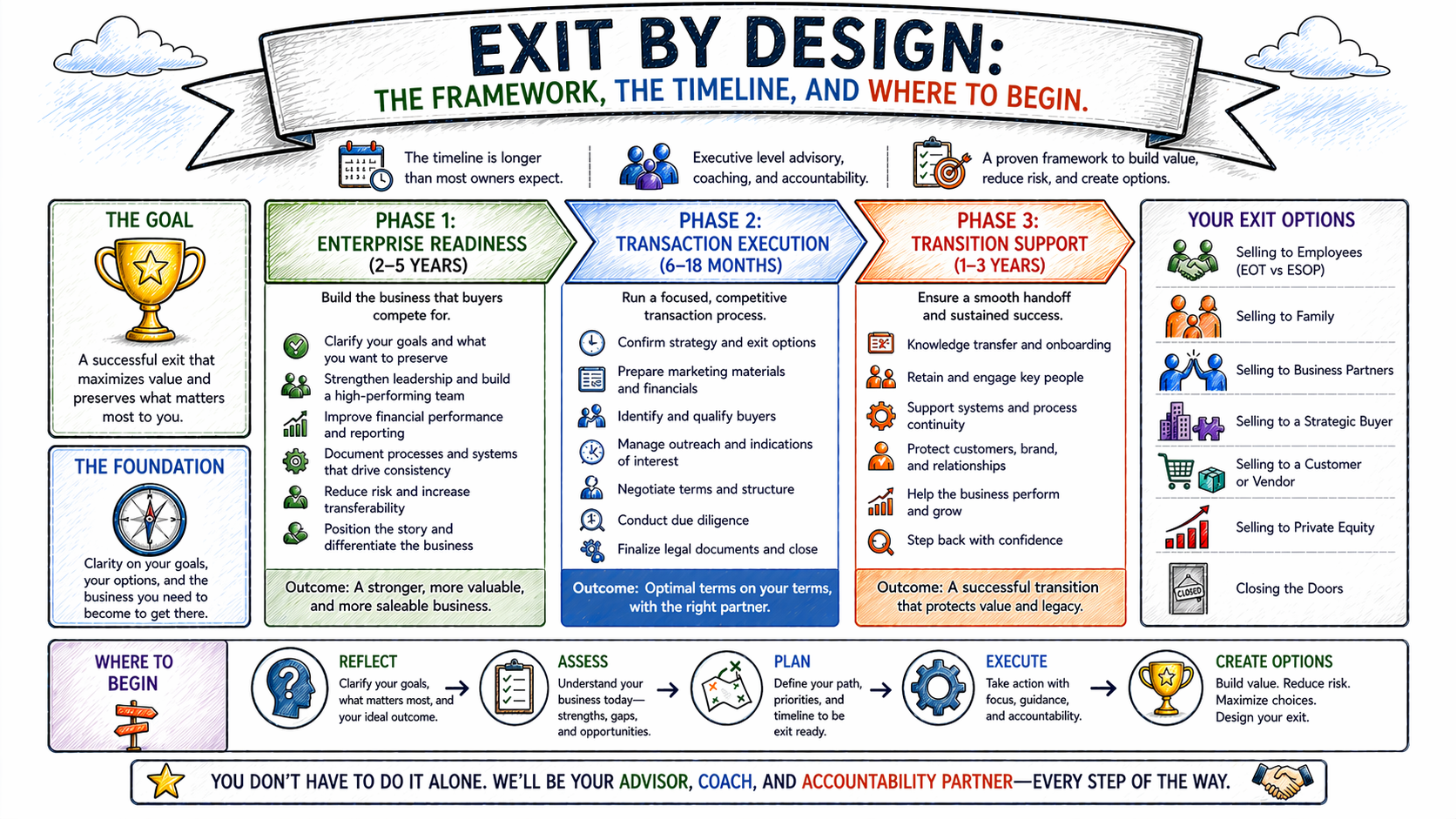

A realistic exit timeline for a government contracting business has three distinct phases, and together they span a decade or more for owners who are executing the process deliberately.

Phase One: Enterprise Readiness

Two to five years before a transaction

This is the foundational phase. The work here is not transaction preparation; it is enterprise development. Distributing decision authority. Documenting institutional knowledge. Building leadership depth below the founder level. Strengthening governance cadence and accountability structures. Reducing customer and contract concentration where possible. Addressing the structural dependencies that would surface as liabilities in a diligence process.

Most of this work improves the business operationally before it improves it transactionally. The owner experiences less friction, cleaner decision flow, and stronger leadership alignment. The enterprise readiness is a byproduct of running a more disciplined organization.

Phase Two: Transaction Execution

Six to eighteen months

This phase begins when the owner engages advisors, prepares the business for market, and initiates the transaction process. It includes financial preparation, quality of earnings analysis, management presentations, buyer identification and outreach, diligence, negotiation, and closing.

For owners who completed Phase One, this phase is substantially less stressful and produces materially better outcomes. The diligence process surfaces fewer surprises. The business presents cleanly. The leadership team can credibly speak to how the organization operates without the founder.

For owners who did not complete Phase One, this phase is where the structural dependencies that were never addressed become negotiating leverage for the buyer. Lower valuations, earnout structures, escrow holdbacks, and indemnification provisions are the most common mechanisms through which structural risk is repriced at closing.

Phase Three: Transition Support

One to three years post-close

Most transactions include a transition period during which the selling owner remains involved in some capacity, including supporting customer relationships, assisting the incoming leadership team, and ensuring continuity of key programs and personnel. The length and nature of this involvement vary significantly by transaction structure and buyer type. For owners who built enterprises with strong operational independence, this period is shorter and less demanding. For founders whose businesses depend heavily on personal involvement, the transition period is longer, and the risk of value erosion is higher.

The full arc from the beginning of enterprise readiness work to the end of the post-close transition period routinely lasts 10 years or more for owners who execute the process deliberately. This is not a counsel of delay — it is a counsel of realism. Owners who understand the timeline plan accordingly. Owners who do not tend to compress the preparation into the transaction phase, where the cost of that compression is measured in deal terms rather than in time.

What the Work Actually Looks Like

Phase One is where Corvata does most of its work with government contracting owners, and it is worth being direct about what that work involves.

It does not involve installing a standardized program or implementing a prescribed toolset.

There is no universal software that solves the structural problems of a founder-dependent GovCon business, and there is no checklist that applies equally to every firm across every market and every stage of maturity.

Two similarly structured businesses can reach the same level of enterprise readiness using entirely different tools and processes, because the tools are not what produce the outcome.

What produces the outcome is structural discipline: clarity about how decisions are made and who owns them, documentation of institutional knowledge that would otherwise leave the business when the founder does, governance cadence that keeps the leadership team aligned without requiring constant founder intervention, and accountability structures that make execution visible and reliable.

The work is not about preparing to leave. It is about building an organization that does not require you to stay.

Corvata helps leadership teams see where those conditions are absent, understand the structural patterns that created the gaps, and build the discipline required to close them, using whatever approaches fit the specific organization. The advisory relationship is not a consulting engagement with deliverables at the end. It is an ongoing working relationship in which the advisor helps leadership make better decisions about the enterprise over time.

The result is not a binder. It is a more durable business.

Preservation Goals Shape the Path Forward

The work of Phase One also provides the space and the clarity to examine the preservation question from Part 5 of this series: what do you actually want to survive the transaction?

That question has real implications for how Phase One is structured. An owner who wants to exit through employee ownership needs to prioritize management development and earnings sustainability. An owner pursuing a strategic sale needs to focus on the structural conditions that affect buyer confidence during diligence. An owner considering private equity needs to address management depth and contract concentration specifically, because PE buyers evaluate both with particular rigor.

Phase One, done well, is not generic enterprise improvement. It is enterprise improvement aimed deliberately at the outcome the owner has defined.

Where to Begin

The most common version of this conversation involves an owner who already knows, on some level, that the business relies too heavily on their personal presence. They can feel the operational friction that comes from undistributed authority. They recognize that certain decisions only move when they are in the room. They understand that the institutional knowledge most critical to the firm lives in their memory rather than in any documented system.

They have not started the work because it has not felt urgent and because the nature of the work is less obvious than that of most operational problems.

Strengthening enterprise structure is not a project with a clear deliverable and a finish line. It is a discipline built over time.

The place to begin is with an honest assessment of the enterprise as it actually operates, not as it appears on an organization chart. That assessment reveals where authority is genuinely distributed and where it is concentrated, where institutional discipline is present and where informal habit is carrying the load, and where the structural gaps are most likely to affect the outcome of an eventual transition.

From that starting point, the path forward becomes visible. The options remain open. And the work of building a business worth transferring can begin on the owner’s terms, in the owner’s time, rather than under the pressure of circumstances no one planned for.

Exit by design does not begin with a decision to sell. It begins with a decision to build something that can stand on its own.

That decision can be made today, regardless of where the owner is in their journey, and the earlier it is made, the more it shapes the journey’s outcome.

The best time to begin this work is before the moment requires it. The second best time is now.

Corvata works with government contracting owners who are ready to take an honest look at the enterprise they have built — what is working, where the structural gaps are, and what it would take to build something genuinely transferable. That work starts with the Corvata Enterprise Readiness Assessment™: a structured evaluation of how your organization actually operates and what would need to be true for exit by design to be a real option, not just an aspiration. If you are ready for that conversation, we are.