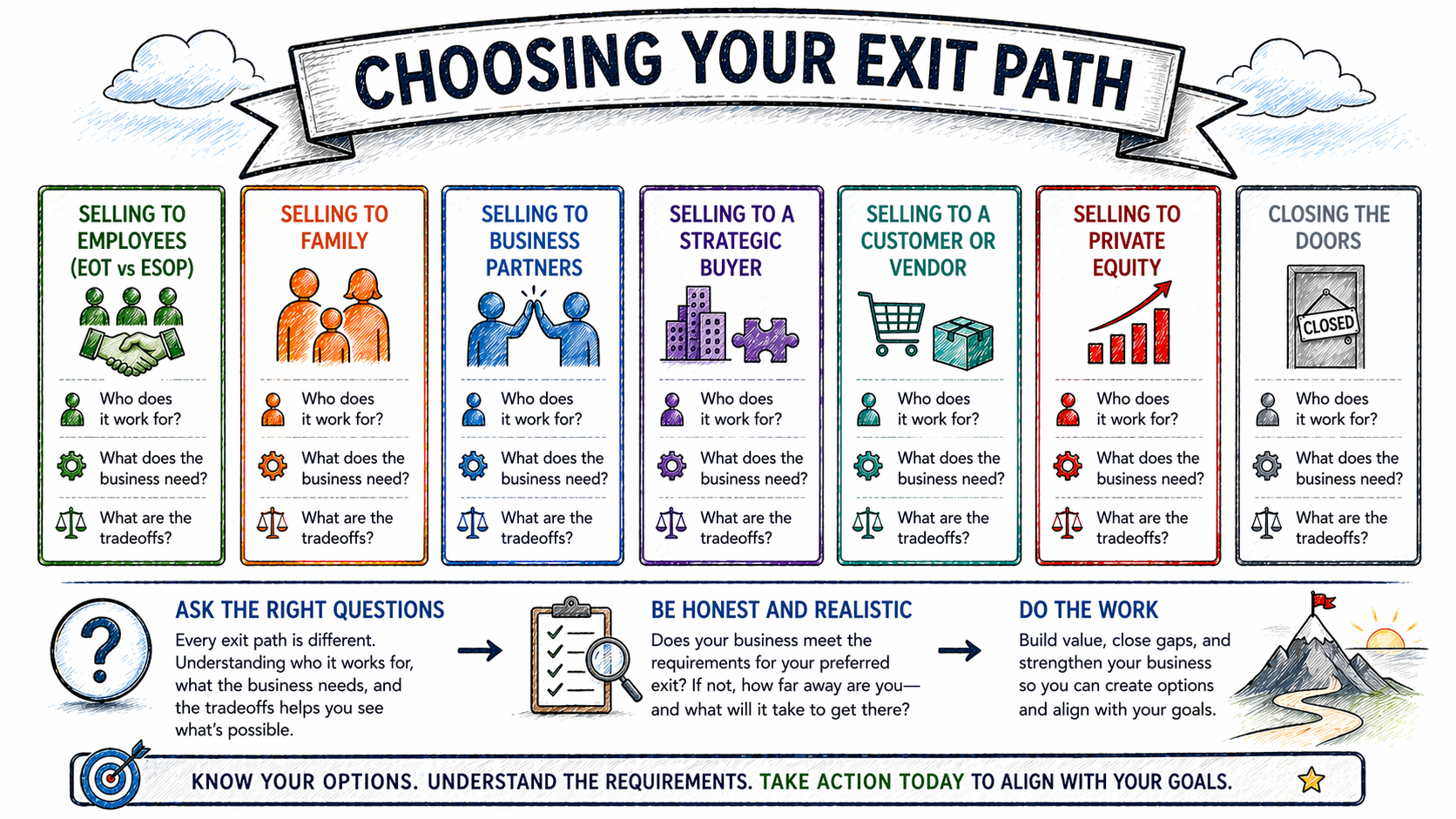

Part 3 of this series introduced the six primary exit paths available to government contracting owners. This post goes deeper. For each path, we examine who it works best for, what structural conditions the business must meet, and the tradeoffs an owner should understand clearly before committing to a direction.

No path is inherently better than the others. Each one is the right answer under specific circumstances and the wrong answer under others. The goal here is clarity, not advocacy.

Employee Ownership

Who it works best for

Owners who have built a strong employee culture and want to preserve it. Owners who want a transaction that does not require finding an outside buyer. Owners with a meaningful tax liability on the sale proceeds who want to explore mitigation structures. Businesses with consistent earnings and an employee base that understands and values shared ownership.

What the business needs

Sufficient and stable earnings to service the financing required to purchase owner equity over time. A management team capable of running the business without the founder’s daily presence. Clean financials, documented processes, and governance structures that can support the transition. In an ESOP specifically, a willingness to operate within the regulatory requirements of a qualified retirement plan.

The tradeoffs

Employee ownership transactions are often slower and more complex to execute than a direct sale. The valuation is typically based on a formal independent appraisal rather than competitive market dynamics, which means the price may be lower than what a strategic buyer or PE firm would pay. The owner’s liquidity is often phased rather than immediate. And the business must have the operational maturity to perform without concentrated founder authority — which is a requirement many GovCon firms have not yet met.

Employee ownership is not a charitable transfer. It is a structured transaction that requires the business to earn its way through the transition.

Family Succession

Who it works best for

Owners with a family member who has been genuinely developed as a leader, not simply designated as one, and who has the capability and the desire to run the business. Owners for whom legacy, continuity, and keeping the business in the family are primary objectives, sometimes ahead of maximizing financial return.

What the business needs

A successor who has operated within the business long enough to understand it, earned credibility with the leadership team, and demonstrated the judgment required to run it. Governance structures that separate family relationships from business decisions. Financial terms that the business can support post-transition without being burdened by debt that was structured primarily around the owner’s liquidity needs.

The tradeoffs

Family succession is emotionally complex in ways that most other transaction structures are not. The conflation of family relationships and business authority creates friction that clear governance and formal agreements can mitigate but rarely eliminate. Valuation disagreements between the owner and the successor, financing structures that depend on post-transition performance, and the difficulty of genuine leadership preparation versus inherited title are the most common failure points. Owners who prioritize maximum financial return will almost always find a better outcome through a different path.

Partner Buyout

Who it works best for

Multi-owner businesses where one or more partners want to exit while others want to continue. Situations where the business is not ready or positioned for an outside transaction but one partner’s circumstances have changed. Businesses where the remaining partners have the financial capacity — or access to financing — to purchase the departing partner’s interest at a fair value.

What the business needs

A buy-sell agreement that was drafted in advance, specifies a valuation methodology, and defines the financing structure for the buyout. This is the most commonly missing element. Without it, the transition that should be the most straightforward often becomes the most contentious. Partners who have operated together for years frequently discover at the moment of transition that their assumptions about valuation differ significantly.

The tradeoffs

A partner buyout keeps the business intact and in operating hands, which is often the cleanest outcome for customers, employees, and contracts. The risk is that the buyout is financed in ways that burden the remaining business, or that the valuation dispute damages the partnership before the transaction is complete. The governance gap — the missing buy-sell agreement — is a solvable problem that most partners defer until it is urgent, at which point solving it is far more expensive.

Strategic Sale

Who it works best for

Owners seeking maximum financial return and who are prepared for the culture and operating independence of the business to change post-close. Businesses with contract vehicles, cleared personnel, past performance records, or customer relationships that a strategic buyer cannot replicate quickly. Owners who are ready for a clean exit and are not primarily focused on what happens to the business after the transaction closes.

What the business needs

A business that can be evaluated clearly by an outside party: clean financials, documented processes, distributed decision authority, and a management team that does not collapse when the founder is removed from the equation. Strategic buyers conduct rigorous diligence. The structural dependencies that are invisible in normal operations become visible — and become negotiating leverage for the buyer — during that process.

The tradeoffs

The financial outcome can be the strongest of any exit path. The post-close outcome for the business is often the least predictable. Strategic acquirers acquire to integrate, and the timeline for absorbing the acquired firm is usually compressed. Brand, culture, operating independence, and sometimes specific programs or customer relationships do not always survive the integration intact. Owners who care deeply about preservation of what they built should weigh this carefully against the financial upside.

Private Equity

Who it works best for

Owners who want liquidity now but are not ready to fully exit operations. Businesses with strong growth potential that could benefit from capital, professional management infrastructure, and operational support. Owners who are comfortable with a defined investment horizon and a subsequent transaction in three to seven years — and who see a second liquidity event as part of the total outcome.

What the business needs

PE buyers are among the most demanding evaluators of enterprise structure. Contract concentration is scrutinized. Management depth below the founder is evaluated carefully. Cleared workforce retention, customer dependency, and the sustainability of financial performance without the founder’s direct involvement are all examined. Businesses with unresolved structural dependencies tend to receive lower valuations, more onerous representations and warranties, or earnout structures that shift risk back to the seller.

The tradeoffs

PE ownership brings capital and operational resources that many GovCon firms cannot access otherwise. It also brings an investment thesis, a return expectation, and a timeline the owner does not fully control after the close. The culture and operating cadence of the business often shift meaningfully under PE ownership. Founders who retain operating roles frequently report that the experience of running a PE-owned business is materially different from running their own. Understanding those dynamics before signing is not optional.

Planned Closure

Who it works best for

Owners of businesses that are genuinely non-transferable in their current form, where value is so concentrated in the founder’s personal relationships and judgment that no transaction structure can effectively transfer it. Owners for whom a managed wind-down on their own terms, while the business is still performing, produces a better personal financial outcome than a forced or distressed sale.

What the business needs

Honest assessment. The decision to pursue a planned closure rather than a sale is often the right one, but it requires the owner to evaluate the business clearly rather than optimistically. The question is not whether the owner believes the business is valuable. It is whether a buyer exists who would pay for that value and whether the value can survive the transfer of ownership.

The tradeoffs

A planned closure forfeits the enterprise value of the business as a going concern. Employees face transition. Customer relationships end or move. The legacy the owner built does not have a successor. These are real costs. They are worth weighing against the alternative: a distressed or deeply discounted sale that produces a worse financial outcome and a worse outcome for the people involved, simply because the owner held on to the idea of a transaction longer than the business could support it.

The Decision Before the Decision

Across all six paths, the pattern holds: the owners with the most options at the moment of transition are the ones who understood their options early, built the structural conditions each path requires, and made deliberate choices about what they wanted to preserve.

That work — building decision discipline, distributing authority, documenting institutional knowledge, developing leadership depth — is not exit preparation. It is enterprise development. The exit readiness is a byproduct of running a better business.

Part 5 of this series examines the question that sits underneath the choice of path: what do you actually want to preserve after the transaction closes, and how does that answer change which path makes sense for you?

Every path has requirements. The question is whether your business meets them — and if not, how far away it is.

Corvata works with government contracting owners to assess enterprise readiness across the structural dimensions that each exit path demands: decision authority, leadership depth, institutional documentation, governance, and contract concentration. If you are beginning to evaluate which path is realistic for your organization, the Enterprise Readiness Assessment™ is the structured starting point for that analysis.