When Circumstances Decide for You

The previous post in this series made a simple argument: every business owner will eventually exit their business, and the only variable is whether that exit happens by design or by default. This post examines what default looks like.

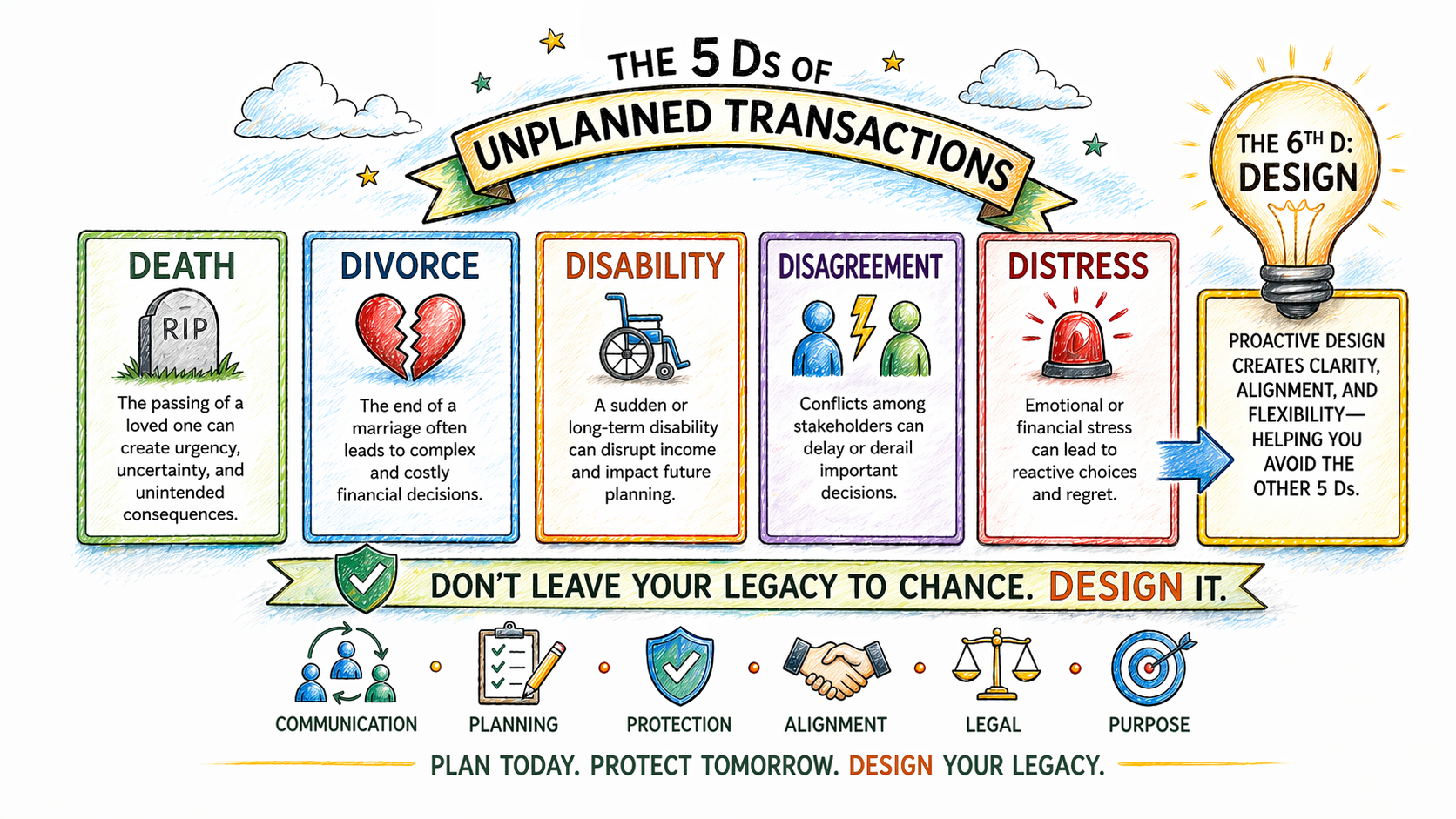

Exit planning professionals have documented five conditions that routinely force ownership transitions before owners are ready. They are not theoretical risks. They are recurring patterns observed across decades of advisory work in privately held businesses that share one defining characteristic: they remove the owner’s ability to control what happens next.

In the government contracting market, where business value is often concentrated in the owner’s relationships, judgment, and institutional knowledge, an unplanned transition carries compounded risk. The structural vulnerabilities that were manageable under stable leadership become acute under pressure.

Death

The most obvious and least discussed of the Five Ds.

Business owners, like most people, resist planning for their own mortality.

The result, in many cases, is an estate that includes a business with no transition plan, no succession structure, and no mechanism for leadership continuity.

For a government contracting firm, the consequences extend beyond the family. Security clearances, contract vehicles, key personnel requirements, and past performance records are all tied to the business’s operating structure. A death that triggers an unplanned change in ownership can put active contracts at risk, create compliance exposure, and reduce the value of the business precisely when the family needs to realize it. It can also result in the spouse or another family member inheriting ownership, creating an uncomfortable situation, as addressed in a previous brief.

A buy-sell agreement funded by life insurance is a standard starting point, but it addresses the financial mechanics rather than the operational ones. The harder question is whether the business can function, and ultimately transfer, without the owner. That question requires a different kind of preparation.

Disability

Temporary or permanent incapacity is statistically more likely than death for owners in their primary working years, and it is less commonly planned for.

A disability that removes the owner from operations for six months does not pause the business. It exposes every structural dependency that normal operations had been concealing.

In a government contracting firm where the owner is the primary decision-maker, the primary customer relationship, and the institutional memory, a sustained absence creates real operational fragility. Decisions that should move through the organization stall. Customers who expect founder-level access begin to question their confidence. Leadership team members who were never given clear authority hesitate to act without it.

The businesses that navigate owner disability with the least disruption are the ones that had already distributed authority, documented decision processes, and built leadership depth before the absence occurred.

Disagreement

Partnership disputes are among the most disruptive and most underestimated risks in privately held businesses.

Co-founders who have built a company together for over 15 years can find themselves fundamentally misaligned on strategy, direction, the pace of growth, or simply on what the business should become.

When disagreement reaches the point of irreconcilability, the options narrow quickly. A forced buyout, a sale of the entire business, or a protracted legal dispute — none of which are conducive to sustaining enterprise value. The businesses that handle partner transitions cleanly are the ones with clear governance structures, documented decision rights, and buy-sell agreements that anticipated the possibility before it became necessary.

Disagreement rarely announces itself. It accumulates quietly, and by the time it surfaces visibly, the governance tools that could have managed it are often absent.

Divorce

In community property states and in marriages where the business represents the primary marital asset, divorce can directly affect business ownership. A settlement that transfers equity to a non-operating spouse, or that forces a liquidity event to satisfy a settlement obligation, can initiate a transition the owner did not choose on a timeline the owner did not control.

This is not an argument about personal circumstances. It is an observation about the intersection of personal and business planning — and the importance of legal and structural clarity around ownership before personal situations create professional ones.

Distress

Financial distress — whether driven by loss of a major contract, a significant compliance violation, a market shift, or a cash flow crisis — can compress the exit timeline dramatically. A business that might have commanded a strong valuation in an orderly sale process is worth considerably less when the owner is negotiating from a position of pressure rather than strength.

In the government contracting sector, contract concentration creates a specific version of this risk. A business that generates sixty or seventy percent of its revenue from a single customer is structurally exposed in ways that may not be apparent until that customer relationship changes.

A distressed sale is not a sale. It is a transfer of leverage from the seller to the buyer.

The Cost of an Unplanned Exit

Across all five conditions, the pattern is consistent. The owner loses control of timing. The business is evaluated under pressure rather than at its best. The structural dependencies that were manageable day-to-day become visible liabilities. And the financial outcome reflects the circumstances of the exit rather than the true value of what was built.

The structural work required to avoid these outcomes is the same work that makes the business more durable today. Distributing decision authority, documenting institutional knowledge, building leadership depth, clarifying governance — none of this is exclusive to exit preparation. It is the work of building an enterprise that does not depend on any single individual to function.

Corvata helps government contracting owners do that work — not through a standardized program or a prescribed toolset, but by helping leadership teams see where their enterprise carries structural risk and building the discipline required to address it. The goal is an organization that can sustain its value regardless of what the circumstances of exit turn out to be.

Part 3 of this series examines the exit options available to GovCon owners and what it means to approach each one from a position of readiness rather than necessity.

The structural conditions that make an unplanned exit more damaging are the same ones creating operational friction today.

If you recognized your business in any part of this post, the right next step is an honest evaluation of where those conditions exist in your enterprise. Corvata’s Enterprise Readiness Assessment™ is designed exactly for that purpose — not to produce a compliance report, but to surface the structural patterns that determine how your organization would hold up under pressure. That conversation starts here.