The Menu Exists. Many Owners Have Never Seen It.

The first two posts in this series established a straightforward premise: every business owner will exit, and the Five Ds represent the most common ways that exit happens before the owner is ready. This post turns toward the alternative: what it actually looks like when an owner exits by design.

Exit by design begins with understanding the options. Not in the abstract, and not only when a transaction is imminent, but early enough that the choice of path can inform how the business is built and structured in the years preceding the transition.

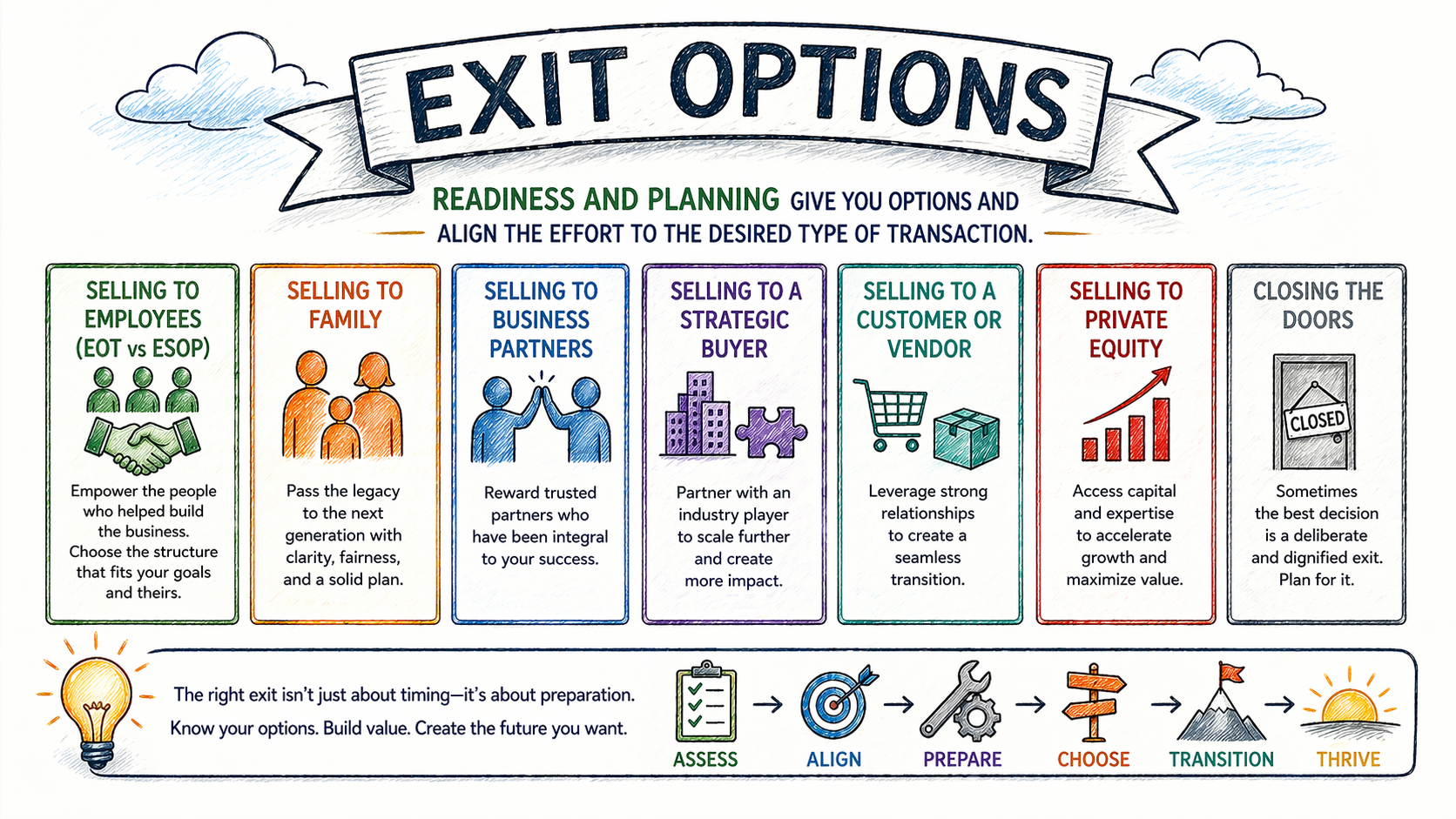

There are six primary exit paths available to government contracting owners. Each produces a different outcome for the owner, for the employees, for the culture, and for the business itself. None of them is universally superior. Each one works well under specific conditions and carries its own requirements and tradeoffs. Part 4 of this series will examine those tradeoffs in depth. This post provides the map.

Selling to Employees

Employee ownership takes two primary forms in the United States: the Employee Stock Ownership Plan, commonly known as an ESOP, and the Employee Ownership Trust, or EOT. Both structures transfer ownership to the workforce, but they operate differently and carry different implications for tax treatment, governance, and the pace of transition.

An ESOP is a qualified retirement plan that holds company stock on behalf of employees. It can be structured to provide the selling owner significant tax advantages while creating a liquidity event that does not require finding an outside buyer. An EOT is a newer structure in the U.S. market — more established in the United Kingdom — that holds the business in trust for the benefit of employees, with different governance and distribution mechanics.

Both paths tend to appeal to owners who have built strong employee cultures and want to preserve them. They are also frequently misunderstood.

Employee ownership is not a charity.

It requires a business with sufficient earnings to support the transaction structure, and it requires operational discipline that allows the business to function without founder-level daily involvement.

Selling to Family

Family succession is often the first exit path an owner considers and the most emotionally complicated to execute. The appeal is clear: the business stays within the family, the legacy is preserved, and the transition can unfold gradually. The challenges are equally clear: valuation disagreements, financing structures that depend on the business performing post-transition, and the difficulty of separating family relationships from business decisions.

Family transitions that work well tend to share several characteristics. The successor has been genuinely prepared, not just designated. The governance structure supports the transition rather than leaving it to informal family dynamics. And the financial terms are structured clearly enough that the outgoing owner can exit without the business carrying unsustainable debt to finance the purchase.

Selling to Business Partners

A partner buyout is among the most common exits in multi-owner businesses and among the least formally planned for. When it works, it is clean: a co-owner who already understands the business, its contracts, and its customers purchases the departing owner’s interest under terms established in a buy-sell agreement.

When it does not work, it is because the buy-sell agreement was never drafted, the valuation methodology was never agreed upon in advance, or the purchasing partner cannot access capital at the moment the transition is triggered. The structure of the arrangement matters far more than most owners realize until the arrangement is actually needed.

Selling to a Competitor or Strategic Buyer

A strategic sale to a competitor, a larger government contractor, or a company seeking to enter the GovCon space can yield the highest valuation among exit paths because the buyer is paying not just for the business’s financial performance but also for the strategic value of the combination. Contract vehicles, cleared personnel, past performance records, and customer relationships that would take years to replicate can command meaningful premiums.

The tradeoff is integration. Strategic buyers typically acquire to absorb, and the culture, the brand, and the operating independence of the acquired firm often do not survive the transition intact. Owners who care deeply about what happens to their people and their business after the close need to understand this clearly before pursuing this path.

Selling to a Customer or Vendor

A customer or vendor acquisition is less common but occasionally a strong fit. A major government customer cannot typically acquire a contractor due to procurement regulations, but commercial customers can. A vendor who supplies a critical capability may see a vertical integration opportunity. These transactions tend to be highly specific to the circumstances and require careful navigation of potential conflicts of interest, but they can produce clean outcomes when the strategic rationale is genuine on both sides.

Selling to Private Equity

Private equity has become an increasingly active acquirer in the government contracting market. PE firms typically acquire with a defined investment horizon of three to seven years, a clear operational improvement thesis, and an expectation of subsequent sale or recapitalization. For owners who want liquidity now and a continued operating role, a PE transaction can provide both — along with capital for growth, professional management support, and an eventual second liquidity event.

PE buyers evaluate government contracting businesses with significant rigor. Contract concentration, customer dependency, cleared workforce retention, and management depth below the founder level are all scrutinized carefully. Businesses that have not addressed these structural factors tend to receive lower valuations, more onerous deal terms, or conditional structures that shift risk back to the seller.

Closing the Doors

Planned closure — winding down the business intentionally rather than selling it — is a legitimate exit path that is rarely discussed without stigma. For some businesses, particularly those that are highly founder-dependent and do not carry transferable value without the owner’s continued involvement, a managed wind-down on the owner’s terms may produce a better personal outcome than a distressed sale or a forced transaction.

Understanding this option clearly, and understanding what would make it necessary versus what structural development would make a sale viable instead, is itself a useful exercise.

Readiness Determines Which Options Are Real

The important observation across all six paths is that readiness determines which options are genuinely available. An owner who has not distributed decision authority, documented institutional knowledge, or built leadership depth below the founder level will find that several of these paths are effectively closed. Employee ownership requires operational independence. Family succession requires a prepared successor. Strategic buyers and PE firms both require a business that can be evaluated and operated without the founder.

Exit options are not created at the moment of exit. They are created by the decisions made in the years preceding it.

Part 4 of this series examines each path in closer detail — the conditions under which each one works, the structural requirements it demands, and the tradeoffs an owner should understand before committing to a direction.

Knowing the options is the beginning. Understanding which ones are real for your business is the more important question.

The exit paths that produce the best outcomes share a common requirement: a business with the structural maturity to support them. Corvata works with government contracting owners to assess where that maturity exists and what it would take to build it toward the path that fits their goals. If you are beginning to think about which direction makes sense, we are a useful sounding board at that stage of the conversation.