The Question Most Exit Conversations Skip

The previous post in this series examined the six primary exit paths available to government contracting owners — the mechanics, requirements, and trade-offs of each. That analysis focused on the financial and structural dimensions of the decision. This post addresses a different dimension, one that sits upstream of the path selection and ultimately shapes whether the owner is satisfied with the outcome.

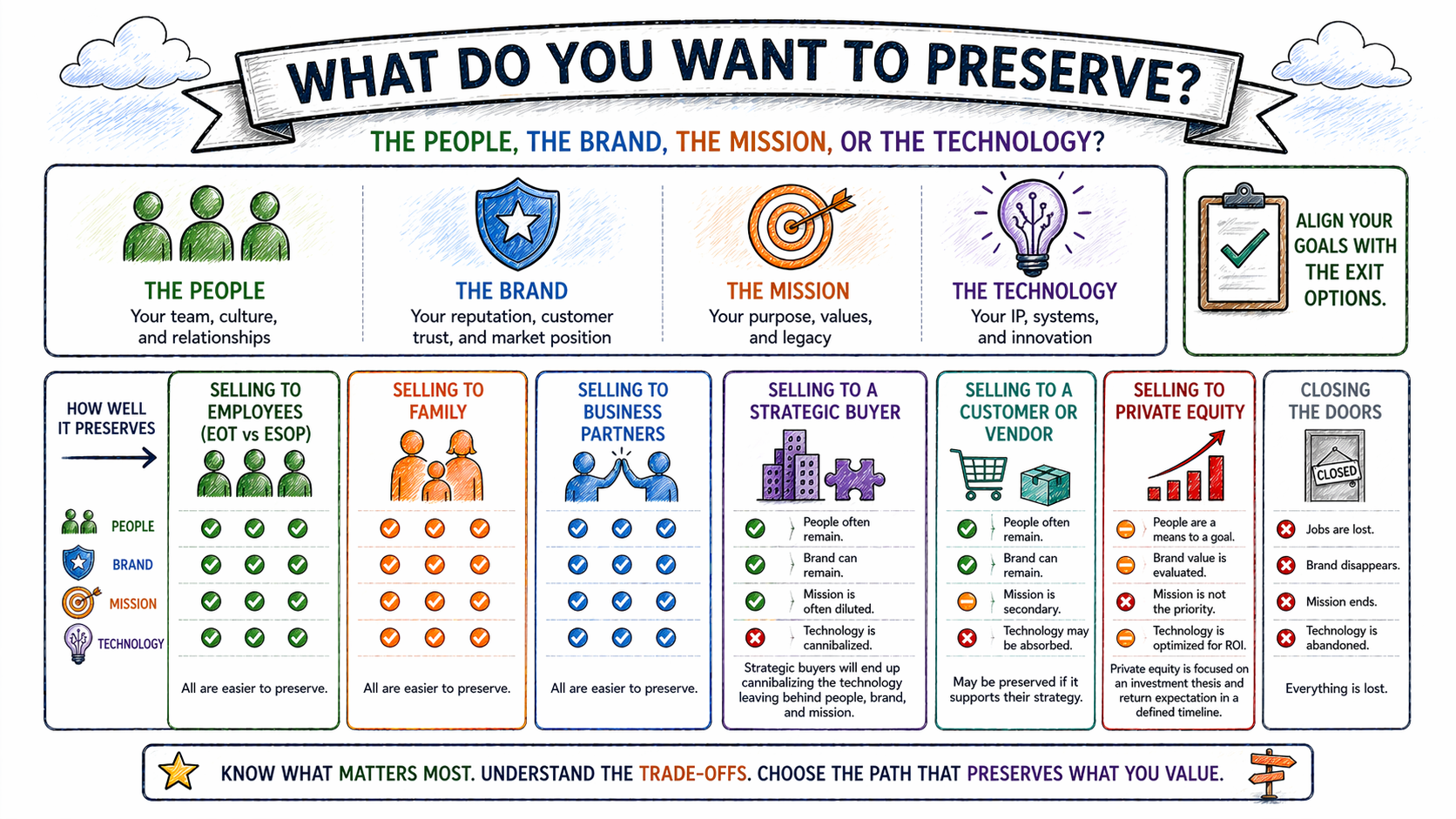

What do you want to preserve?

It is a deceptively simple question. Most owners have a strong instinctive answer. But instinct and intentionality are different things, and in an exit transaction, the gap between them can be significant. Owners who have not thought clearly about preservation goals before engaging in a transaction process often discover — too late — that the structure they chose was not aligned with the outcome they actually wanted.

The choice of exit path is not only a financial decision. It is a decision about what happens to the business, the people, the mission, and the brand after the owner is no longer in the room. Different buyers protect different things. Different structures produce different post-close outcomes. Knowing what matters to you before you engage with any of them is not optional. It is foundational.

The People

For many government contracting owners, the people are the business. The team that grew with the firm, the culture that developed over years, the sense of shared mission that made the work feel like more than a contract vehicle — these are not line items on a balance sheet, but they are real and they are what many owners most want to protect.

Preservation of people and culture is most reliably achieved through employee ownership structures, where the workforce itself becomes the successor, or through family succession, where leadership continuity is maintained within a known and trusted circle. It is least reliably achieved in strategic acquisitions, where integration timelines are compressed and the acquiring organization’s culture tends to dominate.

Private equity transactions occupy the middle ground. PE ownership does not inherently destroy culture, but it changes the operating environment in ways that affect the people within it. Incentive structures shift. Reporting relationships change. The pace and priorities of the business reflect the investment thesis rather than the founder’s vision. Some employees adapt well. Others do not.

If the people are what you most want to protect, the transaction structure and the buyer’s track record with acquired workforces both deserve serious scrutiny before you sign.

The Brand

Brand equity in the government contracting market is more durable and more valuable than many owners recognize. A firm that has built a reputation for performance, reliability, and mission alignment over ten or twenty years has created something that cannot be replicated quickly. Customers who trust the brand return. Partners who know the brand seek collaboration. Prospective employees who recognize the brand apply.

That brand equity does not automatically transfer with the transaction. In a strategic sale, the acquiring firm typically absorbs the acquired brand into its own identity over time. The name may persist on a contract vehicle for a transition period, but the brand’s distinct market presence may not survive integration.

Owners who care about the brand surviving should ask direct questions during the transaction process: What is the buyer’s history with acquired brand identities? Is there a plan to maintain market presence under the existing name? What does the integration timeline look like, and what happens to the brand at each stage? The answers will tell you what you need to know.

The Mission

Some government contracting businesses were built around a specific mission, such as a commitment to a particular customer community, a focus on a specific national security challenge, or a culture of service that the founder considered foundational to the firm’s identity. For these owners, the financial outcome of the transaction matters, but it is not the only measure of success.

Mission alignment is the hardest preservation goal to contractualize and the easiest for a buyer to affirm verbally without honoring operationally. A strategic buyer who speaks the same mission language during the transaction process may have a very different set of priorities eighteen months post-close, when the integration demands of a larger organization take precedence over the commitments made at signing.

The most reliable protection for mission is structural. Employee ownership trusts, in particular, embed mission alignment into the governance of the business itself rather than relying on a buyer’s stated intentions. Where structural protection is not available, due diligence on the buyer’s track record with acquired mission-driven businesses is the next best tool.

The Technology

Technology-driven government contracting businesses often operate on a different exit timeline than the rest of the market, and with good reason. Proprietary technology has a window. The value it commands in a transaction reflects its current relevance, its competitive differentiation, and the market’s confidence that the window remains open. Owners of technology-driven firms frequently understand this intuitively and structure their exit planning accordingly — building toward a transaction while the technology is still at peak value rather than waiting for the broader business to reach a different level of maturity.

For these owners, the preservation question is different. The technology itself is often what the buyer wants most, and the terms of the transaction may reflect that priority directly. The question shifts to what happens to the team that built the technology, whether the buyer intends to continue investing in the platform or to integrate and retire it, and what transition arrangements exist for the technical leadership that made the technology competitive.

Technology exits can produce exceptional financial outcomes. They do not always produce the outcomes the founders hoped for in terms of what happens to the product after the close.

Aligning Goals to Structure

The honest reality of exit planning is that not every preservation goal can be fully achieved in every transaction structure. Maximum financial return and maximum cultural preservation are rarely available simultaneously. The buyer most likely to pay the highest price is often the buyer least likely to maintain the business as the founder envisioned it.

That tension is not a problem to be solved. It is a tradeoff to be understood and made deliberately. The owners who navigate exit with the most satisfaction — financial and personal — are the ones who decided what they were optimizing for before they began the process, rather than discovering their priorities in the middle of a negotiation they could not easily exit.

The question is not what the business is worth. The question is what matters to you, and whether the transaction you are considering can actually deliver it.

Part 6 of this series brings the full arc of Exit by Design together: how the timeline, the structure, and the preservation goals connect into a coherent approach that GovCon owners can begin building toward now — regardless of where they are in the journey.

The owners who exit on their terms are the ones who knew what those terms were before the process began. If Part 5 of this series surfaced a question you have not yet answered with clarity, that is worth sitting with — and worth exploring with an advisor who works exclusively in the government contracting space. Corvata’s conversations typically begin with the owner’s goals and work backward to the structural conditions required to reach them. If you are at that stage of thinking, we would be glad to be part of the conversation.